Medicare Supplement Texas

800-687-8443

Immediate Medicare Supplement Quotes

Pamala and Barry R. - Dallas, Texas

"As you know, since our retirement we have been on a very tight budget. With our Medicare Supplement being one of our biggest expenses each month. We also realize It Is one of our most important. You have always done the best Job in finding the most affordable coverage for Alma and I. We have referred you agency to many of our friends."

"As you know, since our retirement we have been on a very tight budget. With our Medicare Supplement being one of our biggest expenses each month. We also realize It Is one of our most important. You have always done the best Job in finding the most affordable coverage for Alma and I. We have referred you agency to many of our friends."Edgar & Alma D. - Big Spring, Texas

"George and I would like to extend our heartfelt gratitude to you and your staff for all that you did for us with George's last hospital stay. His heart attack came as a complete shock to our family. We are so very relieved to report every last cent was taken care of by Medicare and the Medicare Supplement you recommended to us. It is Agencies like yours that give us the peace we need so we can enjoy our retirement in the fullest possible way."

"George and I would like to extend our heartfelt gratitude to you and your staff for all that you did for us with George's last hospital stay. His heart attack came as a complete shock to our family. We are so very relieved to report every last cent was taken care of by Medicare and the Medicare Supplement you recommended to us. It is Agencies like yours that give us the peace we need so we can enjoy our retirement in the fullest possible way."Pearl & George Z. - Kerrville, Texas

"I can't believe you found me the same Plan F with a different company and saved me $816.00 a year. Thank you very much."

"I can't believe you found me the same Plan F with a different company and saved me $816.00 a year. Thank you very much."Virginia A. - Wichita Falls, Texas

Medicare Supplement Made Easy

A Medicare Supplement Plan is an insurance policy issued by a private company, which "fills in the gaps" left by Original Medicare coverage. A Medicare Supplement insurance can help pay your share of coinsurance, copayments and deductibles. (This is why Medicare Supplement insurance plans are often called "Medigap Plans").

Need help understanding and choosing the right plan?

Original Medicare can be difficult to understand at best and Medicare Supplement insurance plans can be a daunting task! We are here to help! You may be asking yourself, when is the best time to buy a Medicare Supplement insurance policy? The best time to purchase a policy is during "open enrollment", open enrollment is six months prior to your 65th birthday and lasts 6 months from the first day of the month in which you turned 65. This enrollment is extended for those who enrolled in Medicare Part B after the age of 65. During this open enrollment period insurance companies cannot use medical underwriting to turn you down for insurance, make you wait for coverage, or charge you a higher premium. An insurance company also cannot use a pre-existing condition waiting period if you have a guaranteed issue right (also called Medigap protection). For people that are past their open enrollment period you can enroll or change Medicare Supplements any time of the year.

What's next?

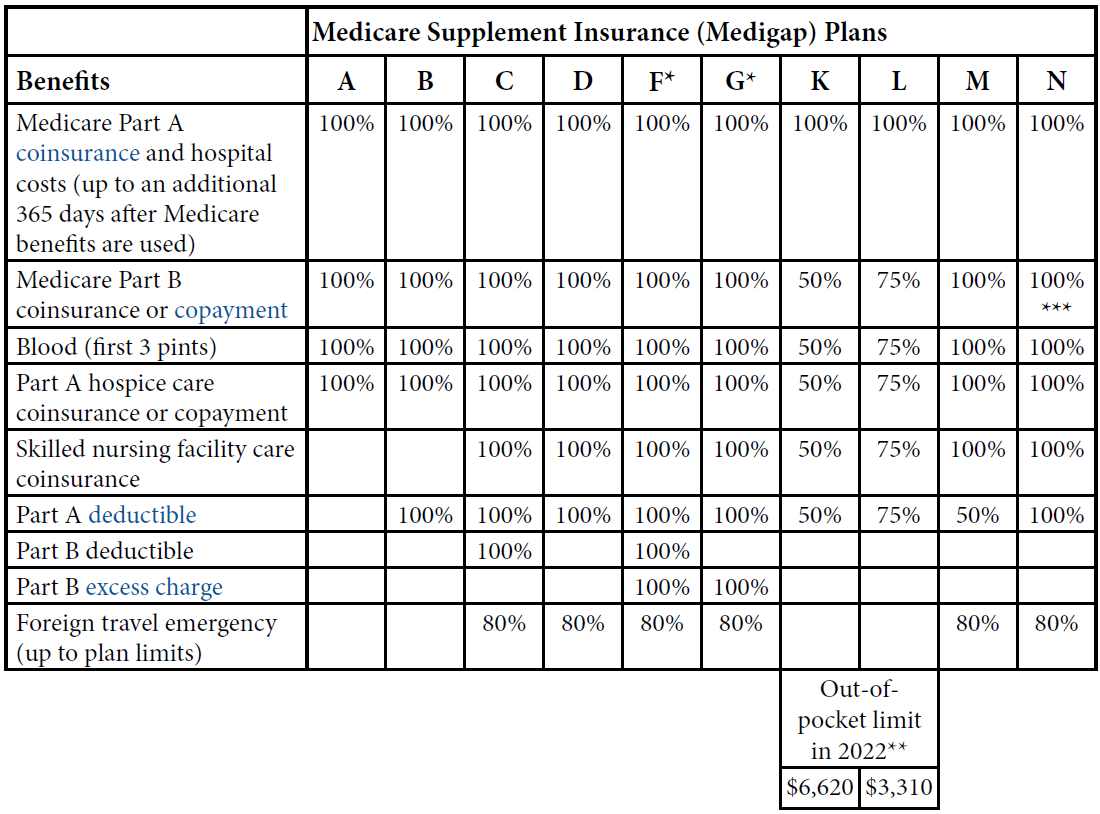

The cost of Medicare Supplement policies vary widely from company to company, there can be huge differences in the premiums that different insurance companies charge for the exact same coverage. Every Medigap policy must follow Federal and State laws designed to protect you and the policy must be clearly identified as "Medicare Supplement Insurance." Medigap insurance companies in most states can only sell you a "standardized" Medigap policy clearly identified with letters A through N. Each standardized Medigap policy must offer the same basic benefits, no matter which insurance company sells it. Cost is usually the only difference between Medigap policies.

What is the most popular plan?

We have found over the years that our customers have chosen the plan "G" more often than any other plan.

Where do I go from here?

First things first, let's think about which benefits you want. You should also think about your future healthcare needs when deciding because you may be unable to switch policies in the future. Below is a chart that outlines the different plans and what they cover.

* Plans F and G also offer a high-deductible plan in some states (Plan F isn't available to people new to Medicare on or after January 1, 2020.) If you get the high-deductible option, you must pay for Medicarecovered costs (coinsurance, copayments, and deductibles) up to the deductible amount of $2,490 in 2022 before your policy pays anything, and you must also pay a separate deductible ($250 per year) for foreign travel emergency services.

**Plans K and L show how much they'll pay for approved services before you meet your out-of-pocket yearly limit and your Part B deductible ($233 in 2022). After you meet these amounts, the plan will pay 100% of your costs for approved services for the rest of the calendar year.

*** Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in an inpatient admission.

Compare Medigap plans side-by-side